Insights on India’s Economy from the CEA

Shall we meet in Bangalore? 🙂

So, in response to last week’s email, one reader wrote back saying, why don’t I share my schedule in advance, so that we can meet up if possible?

And so, I am in Bangalore on the 22nd of April and available to meet up, if you are interested!

- Time: 7.30 pm (22-Apr, Wed)

- Venue: Toit Indiranagar (boy, what a surprise!)

In case you are interested to join, please drop me an email and share your number too. I will form a WhatsApp group to coordinate.

Look forward to meeting you!

And now, on to the newsletter.

Thanks for reading The Story Rules Newsletter! Subscribe for free to receive new posts and support my work.

Welcome to the one hundred and sixty-third edition of ‘3-2-1 by Story Rules‘.

A newsletter recommending good examples of storytelling across:

- 3 tweets

- 2 articles, and

- 1 long-form content piece

Let’s dive in.

𝕏 3 Tweets of the week

Superb way of making that distance relatable. Didn’t know the moon was so far away.

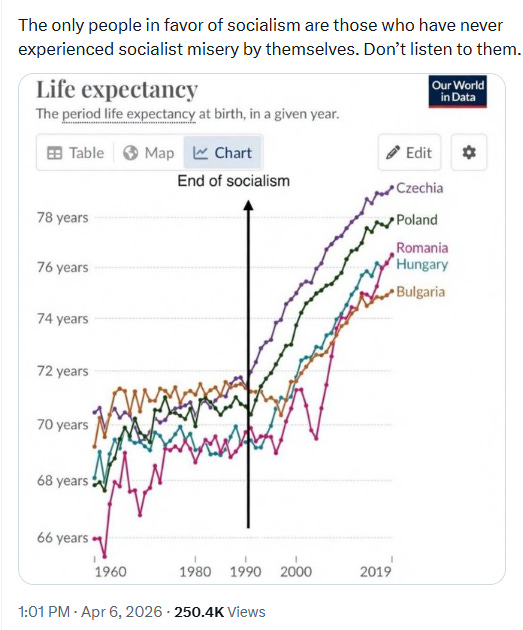

If you think free-markets are bad, always ask, what is the counter-factual?

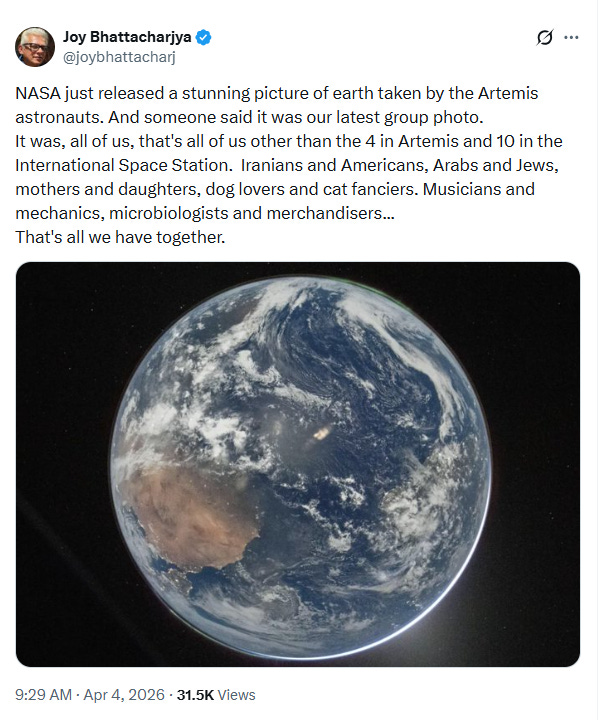

Joy Bhattacharjya has a lovely way with words!

📄 2 Articles of the week

a. Lenny Rachitsky’s biggest takeaways from Anthropic’s Head of Growth Amol Avasare (on LinkedIn)

Some good points made by Lenny from his conversation with Anthropic’s Head of Growth.

Anthropic’s engineers are becoming more productive, and so need more PMs:

With Claude Code, a five-engineer team now produces the output of 15 to 20 engineers. But PM and design productivity haven’t scaled proportionally. The result is a compressed ratio where one PM is effectively managing the output of a much larger engineering team. Anthropic’s growth team is responding in two ways: hiring even more PMs (!), and formally deputizing product-minded engineers to act as mini-PMs for any project with less than two weeks of engineering time.

What AI cannot do—build alignment among stakeholders:

The one part of PM work that AI can’t automate yet: getting six people in a room to agree. Amol and his head of design joke that even with AGI, it’ll still be impossible to align six stakeholders. Cross-functional coordination—managing opinions, navigating politics, mediating tradeoffs—remains the bottleneck that AI doesn’t touch for larger projects. This is why Amol believes PM roles aren’t going away, and may actually grow.

b. ‘Why ‘Cost Disease’ Is the Secret Force Behind America’s Toxic Solitude’ by Alex Mayyasi

I loved this thought-provoking piece that connects a concept from economics (Baumol’s Cost Disease) with the rise of loneliness in the US, and why some sectors like restaurants and cinemas are struggling.

Mayyasi starts with an interesting example of finding a pattern in the data:

Look across the U.S. economy. Cinemas are fighting to stay relevant, but Netflix is a growing juggernaut. Restaurants feel squeezed, but DoorDash has healthy profit margins.

This is a consistent pattern. Companies in the business of bringing people together for shared experiences are struggling. Meanwhile, products that increase the time we spend alone are doing great.

(A counter example might be live events, concerts, travel, etc.?)

Mayyasi’s diagnosis is a concept from economics:

If our social lives seem sick with solitude, that’s because they suffer from a disease with a name. It’s called Baumol’s cost disease.

Mayyasi shares some details about this phenomenon:

Some sectors, such as growing corn and making electronics, have become more efficient and productive thanks to new technology, trade, and automation. But other sectors— especially services, such as haircuts, theater performances, and watching toddlers in daycare—still require as much labor as they did before the Industrial Revolution.

No ballet company can put on 10 Swan Lake performances in the time it used to do just one. Still, in order to keep their workers from switching careers, theaters and childcare centers had to offer higher salaries. And therefore increase their prices. (Sure, many teachers, cellists, and social workers accept lower salaries to do work they love. But if the salary gap gets too big, they will switch.)

Mayyasi frames the social media apps as ‘solitude-inducing’:

The world of digital, solitude-inducing entertainment is scalable, so investors give founders millions to build the next short-form video app, delivery platform, or AI companion company.

Because of cost disease, most of the world’s most powerful corporations and most driven entrepreneurs are well capitalized and incentivized to increase our solitude, while purveyors of long nights with friends are outliers who succeed despite strong headwinds.

He feels that businesses which support social behaviour should be supported:

Cost disease is real, and it has a known cure. Today we’re seeing that one price of a successful economy is the rise of anti-social businesses. But if we want our rising living standards to include friendships and shared experiences—and not just a nation of couch potatoes scrolling on their phones for 10 hours a day—then we’ll need to choose our social future. And pay for it.

🎧 1 long-form listen of the week

Note: I have used AI (Claude Cowork) to create the first draft of this part of the newsletter. I shared the transcript and the themes that I had found interesting, and it pulled out the relevant verbatim portions and cleaned them up for me. The comments are mine (with AI inputs).

This is a superb conversation about India’s current economic challenges and the way forward. I loved Shruti’s sharp, nuanced questions and Nageswaran’s clear responses and rare candour for someone in his position.

Nageswaran evokes Keynes to explain why he changed his mind about import substitution (he was earlier in favour of low customs duties, but now has a changed position):

Nageswaran: Globalization was a cycle which lasted from, let’s say, maybe 1980 until you might say 2015. Then now we have shifted to a phase where countries are weaponizing supply chains, prioritizing domestic production, markets are no longer being neutral, and companies are forced to respond to what their governments tell them to do – whom to sell, whom not to sell, from whom you accept investments.

He uses a vivid line that captures the shift:

Nageswaran: During COVID, even Germany initially was hesitant to supply personal protection equipment to fellow European Union members. As they say, “In a foxhole, there are no atheists.” Similarly, in a crisis, there are no free marketeers.

Nageswaran believes that import substitution and export promotion are not mutually exclusive and that the government can take a sectoral approach to this policy. There are some sectors where import substitution might be needed:

Nageswaran: Import substitution or indigenization, if it is done properly, isn’t incompatible at all with export orientation or quality export competitiveness. In the Economic Survey in Chapter 16, we have given a two-by-two matrix of what is feasible and what is desirable. If it is high feasibility but low desirability, let the market decide. Where it is both feasible and highly desirable, or urgent, from a national security perspective, then of course the state has to actively encourage and catalyze particular production.

Why does India’s private capital expenditure remain stubbornly low? The CEA uses some smart global norm-variance and shares insights on how this is not just an India problem:

Nageswaran: Had COVID not occurred, and with the Government of India cutting corporate income tax in September 2019, it might have paved the way for a big recovery in private sector capex. Then COVID happened, and immediately, the Russia-Ukraine war started, which contributed to oil price increases, supply chain disruptions in semiconductor chips. More importantly, the excess capacity in China and the deflation coming out of that are the biggest concerns because it is not happening only to India. If you look at what is happening to gross fixed capital formation in Thailand, Indonesia, etc., they have been hollowed out. They are even lower than India’s.

This was super interesting – how, because of a generational change within business families, the next-gen is more interested in running family offices (rather than factories):

Nageswaran: You must account for the fact that generational changes in the business families may also lead to less appetite for real investment, but more appetite for financial investment. That is also happening. Obviously, they will not say that. Therefore, it is very easy to externalize the problem.

Did you know that 80% of global equity options are traded in India?!:

Rajagopalan: The Indian financial market has become the single largest equities derivatives market in the world. Something like 80% of global equity options are traded in India, which is quite remarkable for a country of its GDP per capita.

Nageswaran: It very much falls on the side of being a speculative play rather than a hedging play. In some respects, India is under-financialized, whether it is in debt markets, whether it is in financial inclusion. In equity markets, with these derivatives, India is over-financialized for its stage of development.

And Rajagopalan gives an evocative label to this phenomenon:

Nageswaran: The individuals are being sold almost like the ₹10 sachet-type options.

Rajagopalan: Exactly – sachetisation of options.

A rare moment where the CEA openly acknowledges a blind spot – the STT is inadvertently favouring speculation over hedging.

Nageswaran: You have given me a lot to think about on this. I probably haven’t applied my mind as much to the mechanics of the STT being levied on the premium when it comes to options, but on the notional value of the contract when it comes to futures. As you said, it could be having the unintended consequence of reducing the hedging role of futures and encouraging the speculative element. Let me think about it and also probably take back this aspect of the conversation to my colleagues in the revenue department.

A must-listen conversation if you want to know more about India’s economic realities and outlook.

That’s all from this week’s edition.

Photo by Diana Polekhina on Unsplash